Home

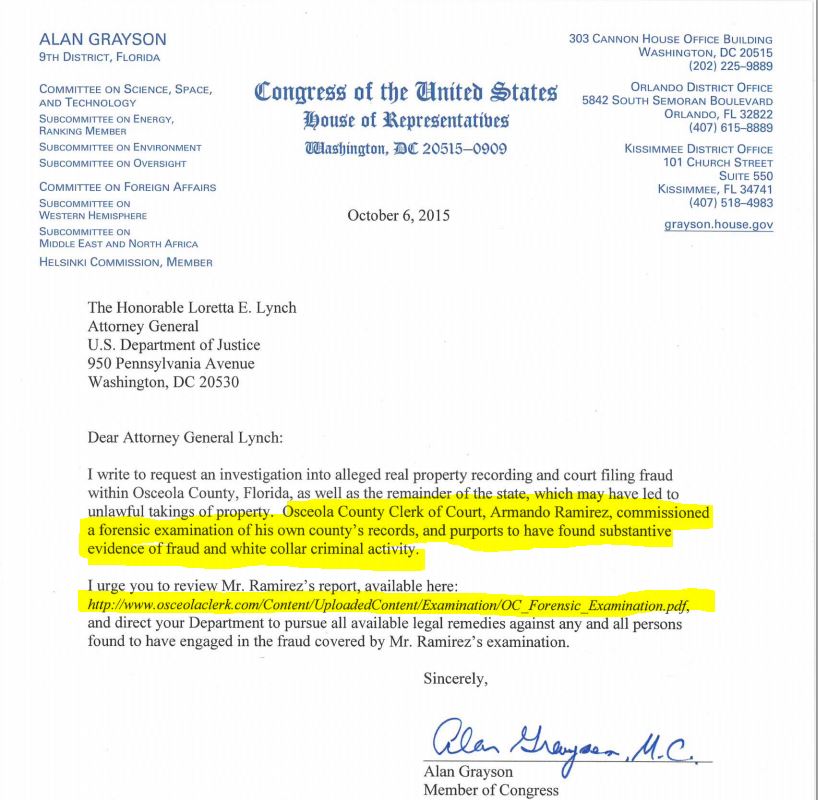

((( Update: See Congressman Alan Grayson letter to US AG Loretta Lynch dated 10/6/2015 at bottom of this page on the same problem Cassino has in Colorado regarding recording of false instruments in county land records. After that is http://osceolaclerk.com/Home/Content/forensic-examination-real-property-osceola-county the FORENSIC EXAMINATION OF THE REAL PROPERTY RECORDS AND THE CIRCUIT COURT RECORDS OSCEOLA COUNTY, FLORIDA )))

This is about Lance Cassino's complaint filed with the CFPB 8/23/2015 Case number 150823-000181 asking for CFPB help in achieving a preferred settlement with JPMorgan Chase (Chase) out of court - instead of settlement by going to court for trial by jury to finally settle this case of almost 5 years including the "partial settlement" of this case at Jefferson County District Court in March of 2013 where Chase paid $10,000 for Cassino's legal fees to dismiss without prejudice their complaint. A Settlement Agreement that Chase had no capacity or jurisdictional standing to enter into - a contract - was recorded at that time which included Cassino applying for a 4th time for a loan modification and to reform the deed of trust from 5 vacant acres by adding to it an adjoining 5 acres with home.

If no preferred settlement is made, taking Chase back to court will be the 4th time in court the last 5 years. This time Cassino seeking a judge's order enforcing his notice of rescission letter sent to on January 30, 2015 soon after the Jesinoski v. Countrywide January 13th, 2015 unanimous Supreme Court decision on how that TILA decision basically allows a "conned/fooled/lied to intentionally" borrower - at their closing - to do something about it. Even past the 3 year TILA statute of limitations due to unknown fraud.

But this is only when and if the borrower learns of the concealment, fraud and likely, non-disclosure of their so called "original" lender resulting in a contract that was never consummated. Again, regardless of the 3 year statute of limitations. a lender when receiving a rescission letter, must file a lawsuit within 20 days to vacate or reverse the rescission, otherwise they lose all rights and interest. Plus the loan, note and deed or mortgage are void - not voidable.

For Cassino's complaint filed 8/23/2015 click on Cassino CFPB Complaint

Below is Chases response 10/14/2015:

This is about Lance Cassino's complaint filed with the CFPB 8/23/2015 Case number 150823-000181 asking for CFPB help in achieving a preferred settlement with JPMorgan Chase (Chase) out of court - instead of settlement by going to court for trial by jury to finally settle this case of almost 5 years including the "partial settlement" of this case at Jefferson County District Court in March of 2013 where Chase paid $10,000 for Cassino's legal fees to dismiss without prejudice their complaint. A Settlement Agreement that Chase had no capacity or jurisdictional standing to enter into - a contract - was recorded at that time which included Cassino applying for a 4th time for a loan modification and to reform the deed of trust from 5 vacant acres by adding to it an adjoining 5 acres with home.

If no preferred settlement is made, taking Chase back to court will be the 4th time in court the last 5 years. This time Cassino seeking a judge's order enforcing his notice of rescission letter sent to on January 30, 2015 soon after the Jesinoski v. Countrywide January 13th, 2015 unanimous Supreme Court decision on how that TILA decision basically allows a "conned/fooled/lied to intentionally" borrower - at their closing - to do something about it. Even past the 3 year TILA statute of limitations due to unknown fraud.

But this is only when and if the borrower learns of the concealment, fraud and likely, non-disclosure of their so called "original" lender resulting in a contract that was never consummated. Again, regardless of the 3 year statute of limitations. a lender when receiving a rescission letter, must file a lawsuit within 20 days to vacate or reverse the rescission, otherwise they lose all rights and interest. Plus the loan, note and deed or mortgage are void - not voidable.

For Cassino's complaint filed 8/23/2015 click on Cassino CFPB Complaint

Below is Chases response 10/14/2015:

Cassino's Protest of Chases Response above was filed 10/27/2015, this is it:

This was CFPB's reply 10/27/2015 to Cassino's Protest of Chases Response above filed 10/27/2015:

Congressman Alan Grayson letter to US AG Loretta Lynch dated 10/6/2015 on this same problem of Cassino in his state regarding recording of false instruments in county land records.

Timely article by Neil Garfield that applies directly to this case:

Rescission Litigation: What to do With that Motion to Dismiss

Posted on October 29, 2015 by Neil Garfield

For more information, please call 954-495-9867 or 520-405-1688

This is for general information only. It is not an opinion upon which you can rely in your case. Get a lawyer. But get one that has really studied this issue because the knee jerk reaction by most lawyers is that rescission cannot be real. Don’t act on anything you read here without consulting an attorney who is licensed in the jurisdiction in which your property is located.

=====================================

I have been receiving requests from pro se litigants and lawyers alike who are now faced with the prospects of early settlements where the rescission “card” has been played — i.e., the “borrower” has filed an action seeking to enforce TILA rescission duties. For the moment, the only thing the banks have come up with to escape the standing problem is to file a motion to dismiss where their standing is presumed since they were sued. But upon closer examination, any motion to dismiss raising defects in the notice of rescission is not properly filed unless the one party in the lawsuit that is actually a creditor, CAN raise the issue. And they can’t raise the issue on a motion to dismiss because the motion is raising facts (like date of consummation) that outside the four corners of the complaint. They cannot even raise the issue in an answer or affirmative defense unless they have real standing (injured party) unless they themselves already filed a lawsuit seeking to vacate the rescission.

We know that the bank lawyers are panicked about rescission. They have put on seminars for each other basically concluding that every point I have been making about rescission is correct and that they are ultimately going to lose unless someone comes up with a credible strategy. The essential problem is that they will not and can not come up with a party who has standing to challenge the the rescission and seek to vacate it through a judicial action (i.e., a lawsuit). And while they have been somewhat successful in the trial courts on some of their efforts to raise issues on motion by raising statute of limitations or other issues, they understand that on appeal, they will lose.

By the way, to the extent their motion to dismiss attacks the rescission, the answer is that the rescission was effective when mailed, by operation of law and that therefore at this moment the note and mortgage are void. And, since they did not file to change anything within the 20 days for compliance, they can’t attack the rescission, so it is permanent. And more importantly they no longer have standing to challenge the rescission because their standing WAS based upon the note and mortgage which are now void instruments. They would need to file an action (lawsuit) seeking to vacate the rescission BEFORE the expiration of 20 days from receipt of rescission (not a motion to dismiss that takes the four corners of the complaint as true). And the party upon whose behalf the action is filed MUST be a CREDITOR in the true sense of the word — not some party holding void instruments, like the note and mortgage.

In my opinion, the proper course of action is to attack the motion to dismiss as an improper use of court procedure to avoid the requirements of pleading. A motion to strike the motion to dismiss would be appropriate. If you accompany that with a memo of law, you will have perfected the record. They want to try to skate by the standing requirement and the small window of opportunity to challenge the rescission and still have the old party who was merely holding paper that is now void file a motion and get rid of the rescission that way.

Judges would like to grant their motion because most of them still believe this is a gimmick by borrowers instead of seeing it for what it is — fraud by intermediaries who have no privity with either borrowers or the investors whose money was used improperly for origination and acquisition of loans (i.e., the REMIC Trust was ignored). The Judges don’t like the result either — the borrower gets a “free house” in their perception and the bank loses out on the loan. Neither assumption is true.

In virtually all cases, the borrower has heavily invested in the property and made many payments and has suffered through years of litigation and opposition to illegal acts by the players who pretend to be lenders or pretend to represent lenders.

Blaming the borrower is completely wrong. The borrower was an unwitting pawn in a game of fraudulent conversion by the banks. And “the bank” loses only some of their investment if they actually paid for the loan or they represent a party who has actually paid for the loan. If they are not creditors and they don’t represent the creditors, where is the harm? If the loan contract actually exists and has been consummated in the legal sense (offer, acceptance and consideration) and if the rescission is valid — they get paid back all the principal they loaned less the fees paid to third parties for origination of an illegal table-funded loan. Where is the harm in that?

It was the borrower who came to the table in good faith, not the banks.

Spread the word

=====================================================================================================================================

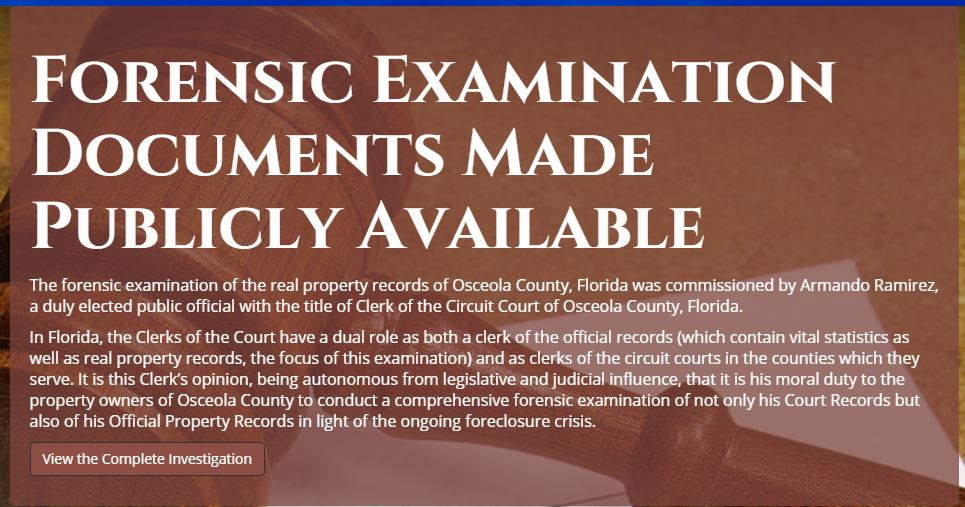

FORENSIC EXAMINATION OF THE REAL PROPERTY RECORDS

AND THE CIRCUIT COURT RECORDS OSCEOLA COUNTY, FLORIDA

December 28, 2014

www.OsceolaClerk.com

(Home Page 10/31/2015)

http://osceolaclerk.com/Home/Content/forensic-examination-real-property-osceola-county

FORENSIC EXAMINATION

OF THE REAL PROPERTY RECORDS AND THE CIRCUIT COURT RECORDS OSCEOLA COUNTY, FLORIDA

Attorney Opinion Statement of Jennifer Englert, The Orlando Law Group, P.A.

December 28, 2014

Armando Ramirez

Clerk of the Circuit Court Osceola County, Florida

2 Courthouse Square Kissimmee, Florida 34741

Dear Mr. Ramirez:

I have been a member of the Florida Bar since 1999. I have defended over one hundred home owners in foreclosure matters and I have seen first-hand how the banks and their servicers have harmed home owners in Florida. I have taken foreclosure cases to trial in Osceola County.

I have been following the actions of Attorneys General of other states with interest to see if they will take any action against those taking homes without the proper paperwork in place. Further, I have been following any cases that address foreclosures to see if there is any relief for homeowners.

While there has not been much in Florida in the way of legislation to assist homeowners in foreclosure matters there are indications and the Legislature does want foreclosures to be done honestly.

Rule 1.110(b), Florida Rule of Civil procedures was amended to require verification of mortgage foreclosure complaints involving residential real property. The primary purpose of this amendment is clearly to provide incentive for the plaintiff to appropriately investigate and verify its ownership of the note and the ability to foreclose on it. It also shows the need to conserve judicial resources that are currently being wasted on inappropriate foreclosures and to avoid harm to defendants resulting from suits brought by plaintiffs not entitled to enforce the note.

Rule 1.110(b) requires a clean, plain statement of accuracy by the person who actually verifies the truth of the claims made, and who is identified as being in a position to actually do so. It would seem that the investigation set forth in the report illustrates many cases in Osceola County alone where the individuals who verified Complaints and supporting affidavits were not qualified to do so or lacked the pertinent knowledge to do so. This alone warrants further investigation.

Throughout the report the Examiner found a clear pattern where “users” of the MERS® System used it to benefit corresponding (originating) lenders, interim funding lenders and warehouse aggregate lenders, who make use of investor money through the pass-through exchange without perfecting the transactions in a timely fashion. Borrowers as well as the applicable government regulatory agencies were unaware notes and mortgages would be converted into image files, to be manipulated and traded within the MERS® System so that no one would know their ultimate path (or whether the loans were fractionalized over multiple trust pools in deviation of GAAP) in the securitization system. MERS appears to have been utilized in RICO-style fashion to coverup the chain of title to make it “fit” into a pattern where the real property records were used to show the path of the mortgage, while the bearer paper (manufactured and manipulated by computer) has been used as evidence in court time after time to foreclose on homeowners. In no other litigation scenario has such unreliable evidence been used on such a regular basis.

Unfortunately members of the bar have been complicit in the efforts of MERS and its users. I am sure the reader is aware of the several attorneys and law firms which have been disciplined and closed due to their behavior in foreclosure litigation as well as the abatement of foreclosure cases due to their behavior. In my fifteen years as a bar member this is unprecedented.

As someone who has dealt with these firms for the past five years I can say that many do their best to hide discovery document, sell notes prior to trial and do whatever else they can to keep defense attorneys from being able to talk to needed witnesses and review the pertinent documents until trial. As Judges have mandates to move these cases along, continuances to get the needed information are virtually non-existent.

The attached report exists to bring light to the abuses of MERS and the court system to improperly foreclose on homeowners. The Examiner found evidence of several statutory violations which will be outlines in the remainder of my letter.

First, in order to perpetuate the scheme of robo-signing and the creation of false affidavits, Florida Statute § 817.15 was violated in that false entries were made to add corporate officers to the books of banks and services with intent to defraud which is a felony of the third degree. These false entries were to create new officers so that they could sign assignments and other documents to allow foreclosures to sail through. Creating false officers also violates Florida Statutes §817.155 and §817.16.

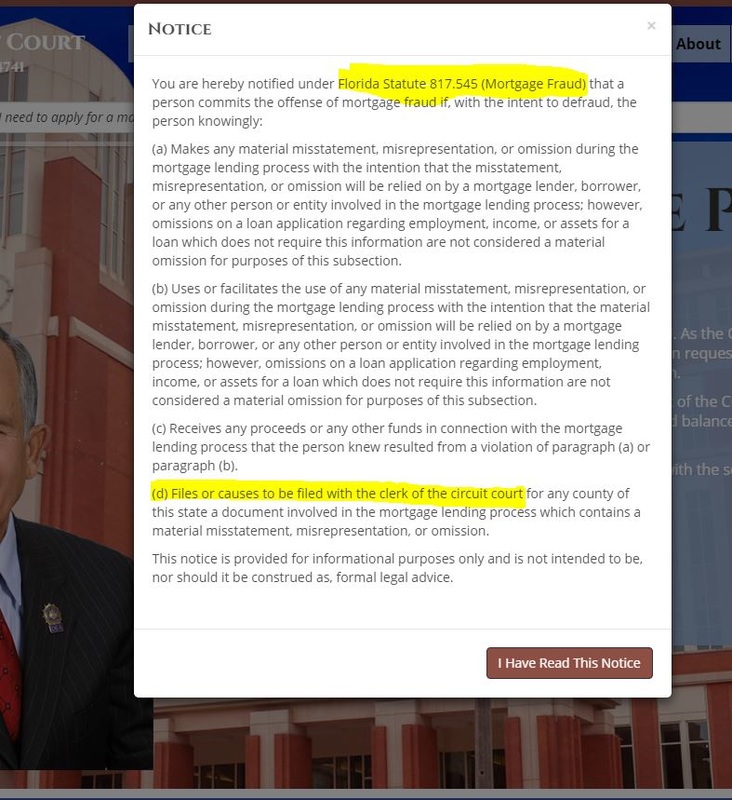

These statutory violations are minor compared to the actions the “fraudulent officers” perpetrated. A highlight of the report is violations of § 817.535 of the Florida Statutes which prohibits filing of false documents or records against real or personal property. A person who files or directs a filer to file false documents with the intent to defraud or harass another commits a felony of the third degree. Repeating this act is a felony of the second degree.

There are also obvious civil penalties which could be addressed with the findings of any criminal investigation which would be a further deterrent to this type of behavior.

The report includes many examples of fraudulent documents which purport to claim under oath that the signor had personal knowledge of the facts attested therein which contained false and misrepresentative information with the intent to deprive the property owner of their property in violation. The “MERS® System” then utilized fraudulent documents to manipulate data in third-party computer software platforms generated and utilized by document manufacturing plants and foreclosure mill law firms to create, manufacture and file documents containing questionable and potentially false and misrepresentative information under the direction of the servicers and title companies to bring fraud on the court.

These actions also consist of forgery in violation of Florida Statutes § 831.01 as MERS, the banks and servicing companies falsely made, altered and counterfeited thousands of public records, in matter wherein such certificate, return or attestation was received as legal proof; with intent to injure or defraud any person, which is a felony of the third degree. By publishing the forged instruments including false deeds, instruments or other writings mentioned in § 831.01knowing the same to be false, altered, forged or counterfeited, with intent to injure or defraud employees of MERS, its users and the applicable law firms were guilty of a felony of the third degree in violation of § 831.02.

The report also outlined statutory violations pursuant to § 117.105 for all the evidence of false and fraudulent notary work based on false acknowledgment on the written instrument which are each felonies of the third degree.

It is clear in the report there is vast evidence of violations of several Florida criminal statutes by MERS, its users and some law firm personnel. From there it is easy to establish under RICO, Florida Statute § 895, an “Enterprise” (a corporation, business trust, or other legal entity)engaged in a “pattern of racketeering activity,” (at least two incidents of racketeering conduct that have the same or similar intents, results, accomplices, victims, or methods of commission or that otherwise are interrelated by distinguishing characteristics and are not isolated incidents.)The Examiner has documented several hundred pages of incidents where documents were falsely created in order to foreclose on homeowners which is a clear pattern of activity. The sole purpose of generating the documents was to have “evidence” to use in a Court of law at summary judgment and trial.

It is practically impossible to poke holes in these documents as they are verified by witnesses who clearly had no role in creating them who simply testify that according to a computer system they can see in their office the documents are genuine.

As a member of the Bar I do hope that action is taken against the manufacturers of false documents as they have been so extensively used to the detriment of so many citizens in our Courts. Had these documents not been so easily available then there would not have been nearly as many foreclosure cases which cluttered dockets and prevented so many from getting a fair trial. All of this is incongruous with our legal system.

Sincerely,

Jennifer A. Englert, Esq.

www.TheOrlandoLawGroup.com

The Forensic Examination Report issued 12/29/2014 and documents are at:

http://www.osceolaclerk.com/Content/UploadedContent/Examination/OC_Forensic_Examination.pdf